According to the IHS company ’s special report on the automotive market, due to the emergence of a large number of safety and accident avoidance applications, automotive technologies that allow communication between vehicles and vehicles and roadside facilities are bound to succeed, although there are still uncertainties about when these applications are deployed .

Speculation on the prospects of automotive-automotive (V2V) and automotive-infrastructure (V2I) technologies shows that in the best case, their potential sales can reach millions by 2015. However, the exact number will depend on which situation is present: conservative, expected, or radical. In each case, there are different specific assumptions that determine the growth rate.

V2V and V2I are collectively referred to as V2X. These technologies allow vehicles to communicate continuously with all other nearby vehicles and road infrastructure, such as traffic lights, campuses, and railway crossings. The communication device may be an embedded telematics system in the car, or a mobile device such as a smart phone.

Many V2X applications will improve safety, vehicle traffic and energy consumption. V2X is also conducive to future cruise-assisted highways and autonomous driving. Therefore, IHS AutomoTIve believes that it is only a matter of time for the V2X system to enter the market, not whether to enter. V2X will be successful in the future, because these systems can greatly reduce traffic accidents while reducing accident-related costs. As long as the installed base of V2V accounts for a large proportion of the number of cars, the above benefits can be realized.

However, due to many market uncertainties, it is difficult to predict the prospects of V2X. Uncertainty comes from global political and economic issues. For example, the US federal budget faces a huge deficit, making it impossible to deploy V2I infrastructure in the near future. Moreover, it is also very complicated to make the V2V deployment order pass the approval process of the European Commission.

To accelerate the deployment of the V2V system, after the initial introduction of the V2V system, a strategy of mandatory deployment will be required. On the other hand, the development of the V2I system will depend on the speed of infrastructure installation and how many cars can communicate with the V2I system. For example, in Japan, there are already infrastructures available to publish traffic information and electronic toll collection.

Because of these uncertainties, both V2V and VSI systems face three different possible prospects.

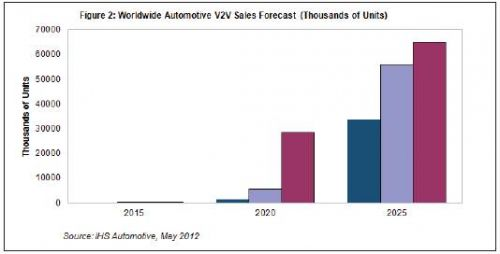

As far as V2V is concerned, a conservative scenario is assumed to be gradually deployed. In 2015, global sales may reach 189,000, including OEM and aftermarket. The market grows steadily every year, but it will not reach the 1 million mark until 2020, and then expand rapidly, reaching 33.7 million by 2025.

In contrast, according to the expected situation-assuming slow deployment but subsequent rapid expansion, it is expected to reach 217,000 in 2015 and increase to 56 million in 2025. The radical situation is similar to the expected situation, but it is assumed that the United States issued a V2V deployment order in 2017, earlier than 2019. Sales in 2015 may reach 351,000, and in 2020 it will reach about 64.9 million.

Figure 2 shows the V2V sales forecasts for 2015, 2020 and 2025 for each hypothetical situation

At the same time, the V2I sales market will be much smaller than V2V, and the deployment speed of V2I infrastructure will be slower than expected. US Department of Transportation research shows that up to 82% of car accidents can be avoided by V2V systems, and V2I technology can avoid another 16% of accidents, which makes deploying V2V systems more cost-effective. The most aggressive V2I forecast shows that sales in 2015 are expected to reach 1,400, increase to 14,500 in 2020, and increase to 58,700 by 2025.

With the development of V2V and V2I technology, V2X will be combined with automatic driving and advanced assisted driving system (ADAS), which may be realized around 2025. It is expected that this will save a lot of costs for society, reduce the cost of crashes caused by property losses, avoid fuel congestion, reduce fuel waste, protect life safety, and many other benefits.

Antenk dip plug connector Insulation Displacement termination connectors are designed to quickly and effectively terminate Flat Cable in a wide variety of applications. The IDC termination style has migrated and been implemented into a wide range of connector styles because of its reliability and ease of use. Click on the appropriate sub section below depending on connector or application of choice.the pitch range from 1.27mm,2.0mm, and 2.54mm here.

IDC DIP Plug Connectors Key Specifications/Special Features:

Materials:

Insulator: PBT, glass reinforced, rated UL94V-0

Contact: phosphor bronze or brass

Electrical specifications:

Pitch: 1.27/2.0/2.54mm

Current rating: 1A, 250V AC

Contact resistance: 30M Ohms (maximum)

Insulation resistance: 3,000M Ohms, minute

Dielectric withstanding voltage: 500V AC for one minute

Operating temperature: -40 to +105 degrees Celsius

Terminated with 1.27mm pitch flat ribbon cable

Number of contacts: 06,08, 10, 12, 14, 16, 20, 24, 26, 30, 32,34, 40, 50, 60 and 64P

With RoHS mark

Used for ribbon cables

DIP Plug Connectors Application

Wire to Board

Apply to Industries : PC, IPC, Consumer Electronics, Automotive, Home Appliance, Medical

Dip Connector,Dip Plug Connectors,Dip Direct Pulg Connector,IDC Plug Connector,Idc connector dip plug,1.27mm Dip Plug Connector,2.0mm Dip Plug Connector, and 2.54mm Dip Plug Connector

ShenZhen Antenk Electronics Co,Ltd , https://www.antenksocket.com