The fierce battle in the autopilot industry looks like a soap opera. The relationship between the characters in the play is tangled up, but the plot is brilliant, and it is absolutely not a dog's blood.

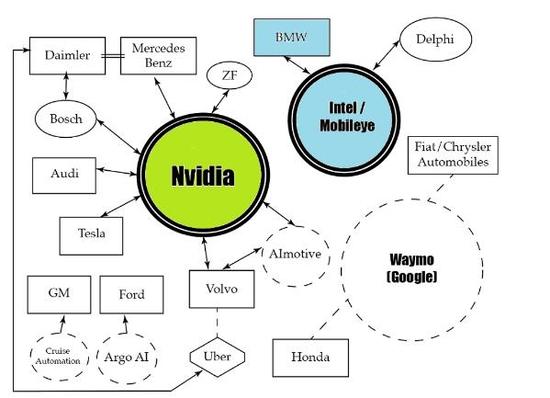

Not long ago, Daimler announced that it had reached a cooperation with Bosch and the two companies will accelerate the mass production of "robo-taxis". In this news, apart from Daimler-Benz and supplier Bosch, there is one company that deserves attention – Nvidia. This company will become a partner of the Daimler-Bosch Alliance Automated Driving Platform.

Mobileye vs. Nvidia

In fact, every time the Level 4 and Level 5 autopilot platforms are mentioned, the entire industry will be divided into two camps, either standing on the side of Mobileye or standing on the side of Infinity. But on the whole, Nvidia's steps are getting faster.

Phil Magney, founder and chief advisor of Vision Systems Intelligence, said in an interview that Daimler was "very pleased after reading Nvidia's road map in the AI ​​and autonomous driving areas."

According to Lei Feng, Daimler subsidiary company Mercedes-Benz has already announced that it will cooperate with Nvidia to develop artificial intelligence-based automatic driving technology before Daimler will join hands with Bosch.

Of course, it is not surprising that Daimler and Bosch chose Nvidia. Last July, old rival BMW and Intel and Mobileye formed an alliance. Last month, Intel bought Mobileye directly. In addition, last year, Intel and Mobileye also brought the first-tier supplier Delphi to the chariot.

In recent months, many German automotive manufacturers have announced their own self-driving car R&D plans, and Nvidia has occupied an important part of them, surpassing Mobileye.

However, Egil Juliussen, head of research at IHS Automotive, believes that Mobileye will likely fight back in the near future and once again overpower Nvidia. After all, Mobileye has a huge advantage in the number of automotive manufacturers and Tier 1 suppliers.

What important information can be revealed in Mobileye's annual report?

Juliussen made this judgment mainly because Mobileye has absolute dominance over the ADAS market. Mobileye has an overwhelming advantage in the amount of computer vision modules installed.

It can be seen from the Form 20-F file that Mobileye submitted to the SEC that, as of the end of last year, Mobileye's modules had entered 15.7 million vehicles worldwide. Mobileye stated: "Already 21 automakers have used our technology, and 25 automakers have chosen Mobileye's products."

At the moment, Mobileye's advantage still belongs to the era of ADAS, but its “can continue this advantage to the autopilot platform remains doubtful.â€

Mobileye's documents submitted to the SEC also show that Mobileye has not stood still in the future platform design. The company has received orders from five automakers focusing on Level 3 autopilot. At Level 4, Mobileye signed five vendors.

* Mobileye co-founder and CTO Amnon Shashua

Many observers in the automotive industry believe that Mobileye can efficiently implement the role of ADAS to autonomous driving. Part of the reason is that this Israeli company "has always been on the path of rapid innovation." Today, this company, which already belongs to Intel, has also invested a lot of resources in the research and development of substantive technology components.

When Intel announced the acquisition of Mobileye, Magney said: "I think Intel believes that the Mobileye team has its own methodology in research and development. In addition to global vision, they have strong localization capabilities." In the eyes of Mobileye, REM (Road Experience Management ) is "an end-to-end map and localization engine for fully automated driving," and by increasing REM, Mobileye can make a lot of money.

R&D projects bloom everywhere

Although various manufacturers have adopted a vertical and horizontal approach, can the friendship between them be long-lasting?

For auto makers, what they need is technology that will enable the company to get a demonstration of a self-driving car by 2020. It is not the purpose of these companies to make money—first realize what they have to say.

Some manufacturers are more interested in new business models. They think that taxis operated by self-driving cars are the future of the industry.

Magney explained that "the city's transportation platform may be the direction of the highest return on investment in the near future, after all, sharing travel represented by Uber has already taken root in many countries." He said. "Urban taxis operate in a simpler environment and are suitable for vehicles that have not yet achieved Level 5 autopilot."

In addition, Magney believes that vehicles equipped with these applications will significantly increase autonomous driving capabilities: Data collection, OTA, and security capabilities will improve significantly. At the same time, however, such capabilities are also prone to redundancy and costly. Although this test can increase the experience, it is very likely to turn the entire project into a scientific experiment. However, such an experiment has no practical value.

Of course, the automakers are not waiting for it. Before the cooperation between Daimler and Bosch, Mercedes-Benz had two teams developing self-driving cars. According to Reuters, the two teams took different paths: one took a gradual route and focused on excavating the potential of conventional vehicles; the other carried out an aggressive transformation of vehicle design to accommodate the needs of future autonomous driving.

Who and who is the family?

In addition to the Mobileye Alliance mentioned above, Nvidia also has many supporters, including the giants Audi and Daimler, as well as the two first-tier suppliers Bosch and ZF. Juliussen believes that these two Tier 1 suppliers are important because they can help Nvidia attract more automakers.

Unlike the alliance of German giants, Americans are more direct. General Motors and Ford Motor Co., Ltd. directly incorporated auto-driving software companies in acquisitions and investments. Last year, General Motors acquired $1 billion in Cruise Automation, and Ford invested $1 billion in Argo AI. The two little-known start-up companies have sold a good price.

On the other hand, Waymo, the first to explore autonomous driving, chose to cooperate with Honda and Fiat-Chrysler. The latter has jointly launched a test vehicle with Waymo, but Honda has not yet done anything.

As the world’s largest automaker, Toyota wants to go it alone—the Toyota Research Institute (TRI) is set up and will invest US$1 billion in robot and artificial intelligence research in the next five years. However, so far Toyota has not come up with its own software or hardware platform.

Gil Pratt, an MIT professor who has already joined TRI, said at this year's CES that we are using the most advanced artificial intelligence available and we are also a bit far behind Level 5 autopilot. Of course, some people think that his remarks are too conservative, but there are also supporters who say that Pratt just said the truth.

Magney said: "Toyota is taking a pragmatic road. After all, before people have changed their minds, Toyota still has to sell cars to make a living."

Most of the other vendors' plans are still blank, but according to Lei Feng Network (public number: Lei Feng Network), on the ADAS system, companies such as Nissan, Hyundai and Kia now use Mobileye's solutions.

It is worth noting that the companies that partnered with Daimler could not only be Bosch and Nvidia, but they also pulled Uber earlier this year. Magney said: "Uber's potential is worth paying attention to, if it can preemptively get the autopilot technology, it will be able to use the existing taxi platform to obtain a huge advantage."

Have these complicated relationships been exhausted? Of course not, we must not forget Tesla, the market value of this electric car manufacturer just beyond GM.

Previously, Tesla was also an ally of Mobileye, but the two companies lost their lives in an accident in Tesla. Therefore, Tesla turned to the Nvidia camp. Magney said: "Tesla's series of actions is indeed commendable. It has built the right architecture from the beginning and now only needs step-by-step software upgrades."

Where are the opportunities for start-ups and automakers?

The autopilot market is not a unique business for automakers, technology companies and tier one suppliers. Other companies can also get a piece of the pie. Juliussen gave us an introduction to the various ways in which these companies can join the corps.

He said that if you are a start-up company that wants to enter the industry, “purchasing electric vehicle batteries, building an image that focuses on building luxurious models, and then buying or developing an autonomous driving platform. After the products are formed, look for a manufacturer to help you Production." This pattern is common in the industry, Zoox, Waymo, and even Apple are the case.

If it is a car manufacturer, Juliussen also provided three suggestions.

First of all, you can develop your own software platform (either through acquisitions or internal teams). Both Ford and GM are on the move.

Second, you can hire a Tier 1 supplier to help you design a self-driving car, such as Delphi to help you build an automated driving platform based on Mobileye products.

For most automakers, this is a proven model. Magney believes that the cooperation between Daimler and Bosch is the best example. The latter has a strong integration capability, and it is absolutely necessary to create a system with a production-grade level.

"Bosch has extensive experience in ECU tuning, and it is also handy for autopilot sensing technology," Magney added. However, Daimler chose Bosch, perhaps also to get in touch with Nvidia from the side, the latter's structure is priceless.

Of course, if you are not an auto giant like Ford or GM, you can choose a third option: buy a third-party autopilot platform from a third party to help third-party manufacturers help with production. If it is really lacking in capacity, it can also focus on the research and development of ADAS vehicles.

Today's automated driving market has already started a two-way battle mode, but the market is still in its infancy.

Magney concludes: “The exploration of various companies is building blocks for the auto-pilot market, but how to integrate the technology into a mature platform is the biggest challenge. The world of automated driving is a layer of 'building blocks' (such as control, No one can master everything, such as safety, behavior and perception, etc. If you want to achieve automatic driving, everyone must form an alliance."

Famous brand A grade Lithium Iron Phosphate Battery Cell

Prismatic Lithium Cell capacity range: 3.2V40Ah, 3.2V50Ah,3.2V100Ah,3.2V206Ah,3.2V277Ah.

1.Long cycle life : normally with more than 4000 cycles life, and can be used for 8 years.

2.Environmentally friendly: it does not contain any metallic chemical element or precious metals and are generally low cost in regarding to materials.

3.Wide operating temperature range:-20℃ ~ 55℃, it is commonly accepted that LiFePO4 Battery cell does not decompose at high temperatures.

4.Light Weight: the volume of the lithium iron phosphate battery of the same specification and capacity is 2/3 of the volume of the lead-acid battery, and the weight is 1/3 of the lead-acid battery

5.Multiple Certification Reports to Ensure Product Safety: CE, IEC, UL, UN38.3, MSDS certified.

Widely application: Mine car, home energy storage, UPS, Solar power, Marine, Camping,Rv, etc, Medium and large passenger cars, logistics vehicles, trucks, forklifts, energy storage power station, etc.

LiFePO4 Cell, Battery Cell, Prismatic Lithium Cell, Lithium ion Cell, Solar Cell

Hangzhou Saintish Technology Co.,Ltd. , https://www.saintishtech.com